SAN BENITO — The San Benito school district’s $223,800, 10-month forensic audit aims much of its focus on a $40 million bond-funded construction project, which led auditors to raise questions.

The audit conducted by the Fort Worth-based firm of Weaver and Tidwell also focuses on credit card expenditures, purchasing and procurement practices, federal funds and grants, payments to vendors and contractors for construction projects and facilities along with payments to consultants and professional services firms from Sept. 1, 2016 to Aug. 31, 2021.

During a meeting late last month, the auditors presented school board members with recommendations aimed at addressing findings.

Last week, Joseph Palacios, the project manager overseeing the construction project, stood behind his work along with the district’s program.

“It was a lot of opinions,” Palacios, a former Hidalgo County commissioner who serves as president of the Brighton Group, the Edinburg-based firm serving as project manager, said, referring to the audit. “There’s absolutely nothing in the findings that says something’s wrong.”

Meanwhile, former Superintendent Nate Carman stated he was “proud” of his work along with the district’s operations during his tenure from late 2017 to March, when he resigned to take a job with the Socorro school district in El Paso.

Late last month, San Benito school board member Janie Lopez told CBS4 News the audit’s findings pointed to a “possibility that laws were broken,” adding, “that would be something that law enforcement would need to further look into.”

Carman “vehemently denied” any such claims, according to Christy Flores-Jones, spokeswoman with the Socorro school district, who spoke on Carman’s behalf last week.

“The scope of the audit was not at any point an investigation of Dr. Carman,” she stated. “Dr. Carman was caught by surprise when media outlets began reporting allegations of a criminal investigation or mentions of criminal activity. To be very clear, these allegations are without merit and Dr. Carman vehemently denies said allegations.”

Flores-Jones went on to say that the audit was based on a review of San Benito school district operations and described the scope as being “predetermined by the board.

“Dr. Carman voluntarily participated in the review with the third-party firm, including participating in interviews and providing requested documentation or information as needed,” she stated, adding Carman was “confident” in his leadership at San Benito.

Auditors also said in a late-September meeting that they found no violations of the law in their review.

CREDIT CARD EXPENDITURES

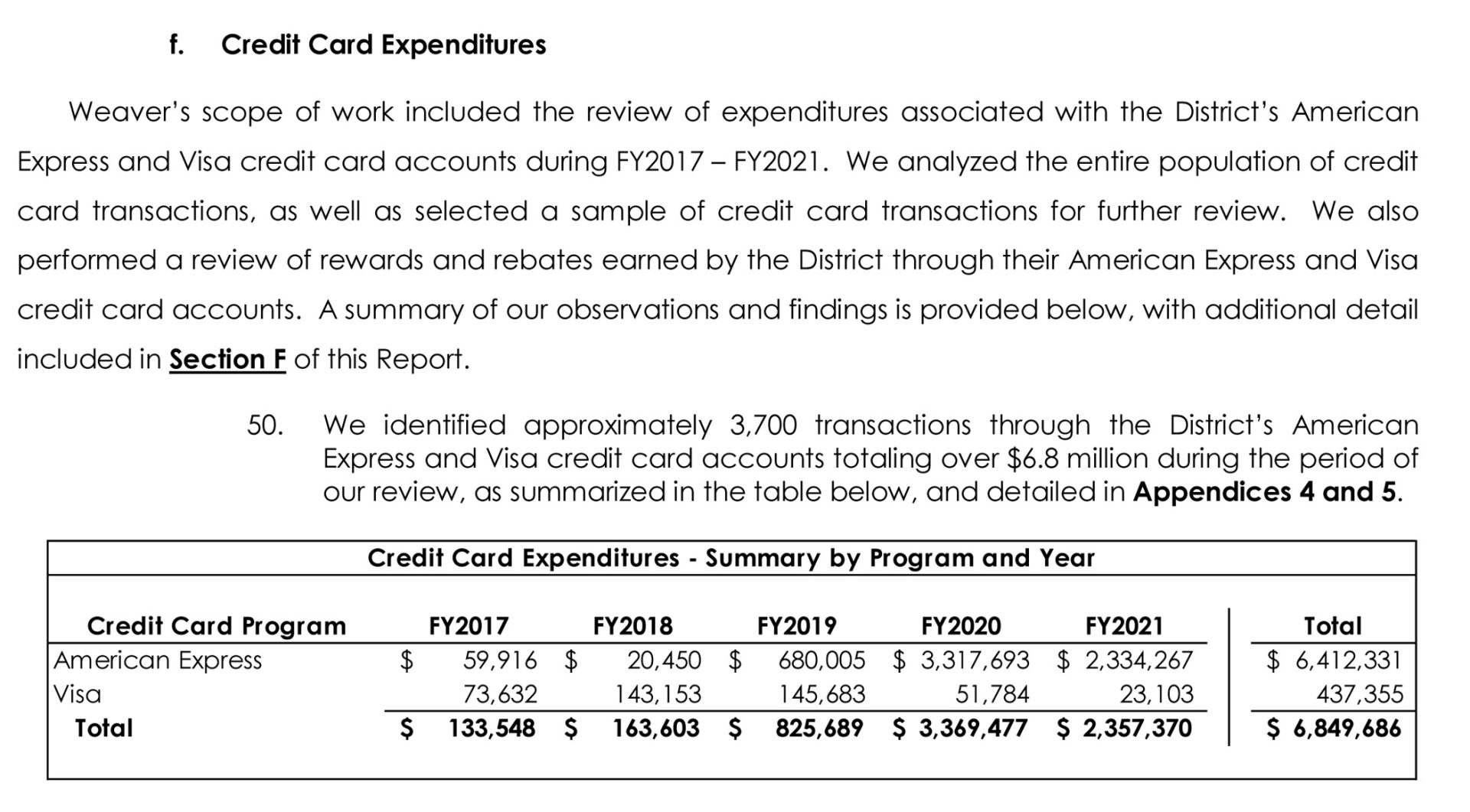

The audit included a review of 3,700 credit card transactions from 2017 to 2021, the report states.

During their review, the auditors found the district earned American Express “additional rebates” from 2017 to 2018, it states.

The audit shows the district redeemed American Express rewards points through cash gifts to the district office totaling $9,325, which was used for a Thanksgiving luncheon, the report states, adding rebates totaled $150,000.

As part of their review, the auditors found three transactions without purchase orders, three without supporting documentation and seven whose documentation was destroyed pursuant to a record retention policy, it states.

During the review, they found 30 instances in which Carman stayed at Marriott hotels during district travel paid with a district credit card, with Marriott rewards points applied to his personal Marriott rewards account, the report states.

The review also found 16 instances in which board members or district employees stayed at Marriott hotels during district travel paid with a district credit card, with Marriott rewards points applied to Carman’s personal Marriott rewards account, it states.

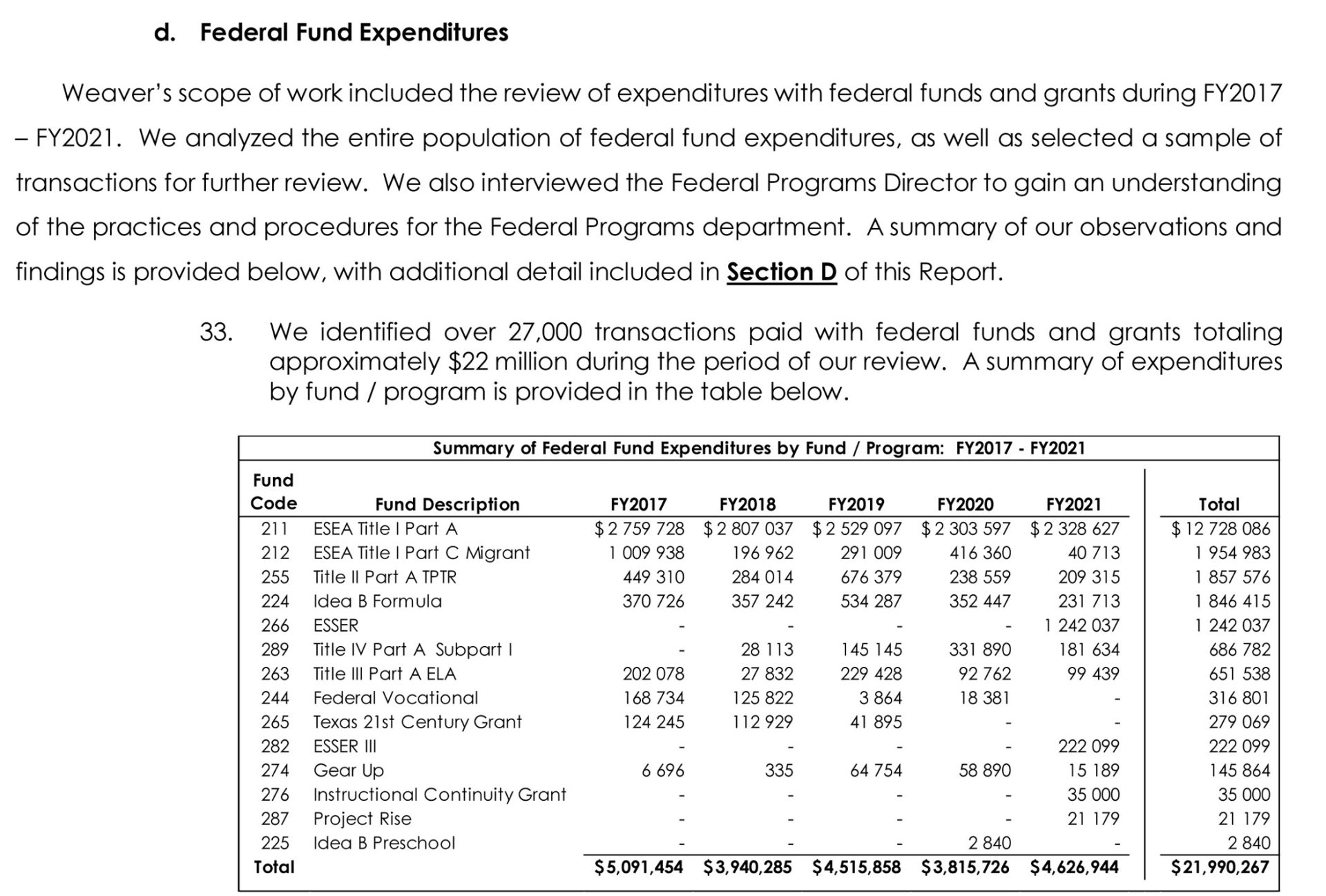

FEDERAL FUND EXPENDITURES

During their review, the auditors found $1.3 million worth of expenditures on the district’s American Express credit card, the report states.

“For eight of the 25 purchases under $50,000, we were unable to determine whether the district obtained multiple quotes,” the auditors wrote.

In 2019, the district procured CMAR services through requests for qualifications as part of the 2018 bond project, the report states.

“It did not appear that the district completed the second step of the CMAR selection process as defined under the Texas Government Code,” it states.

From 2018 to 2019, the district paid vendor Dezvia LLC $78,000 to remodel the central office as part of a project for which the auditors wrote, “it did not appear that other quotes were obtained,” the report states.

The audit included a review of the board’s 2020 appointment of Jeff Everitt & Associates, selected to serve as the district’s insurance agent, it states.

“The insurance agent of record services was not procured through an RFQ process … a possible violation of Texas Education Code Section 44.031,” the auditors wrote.

CONTRIBUTIONS

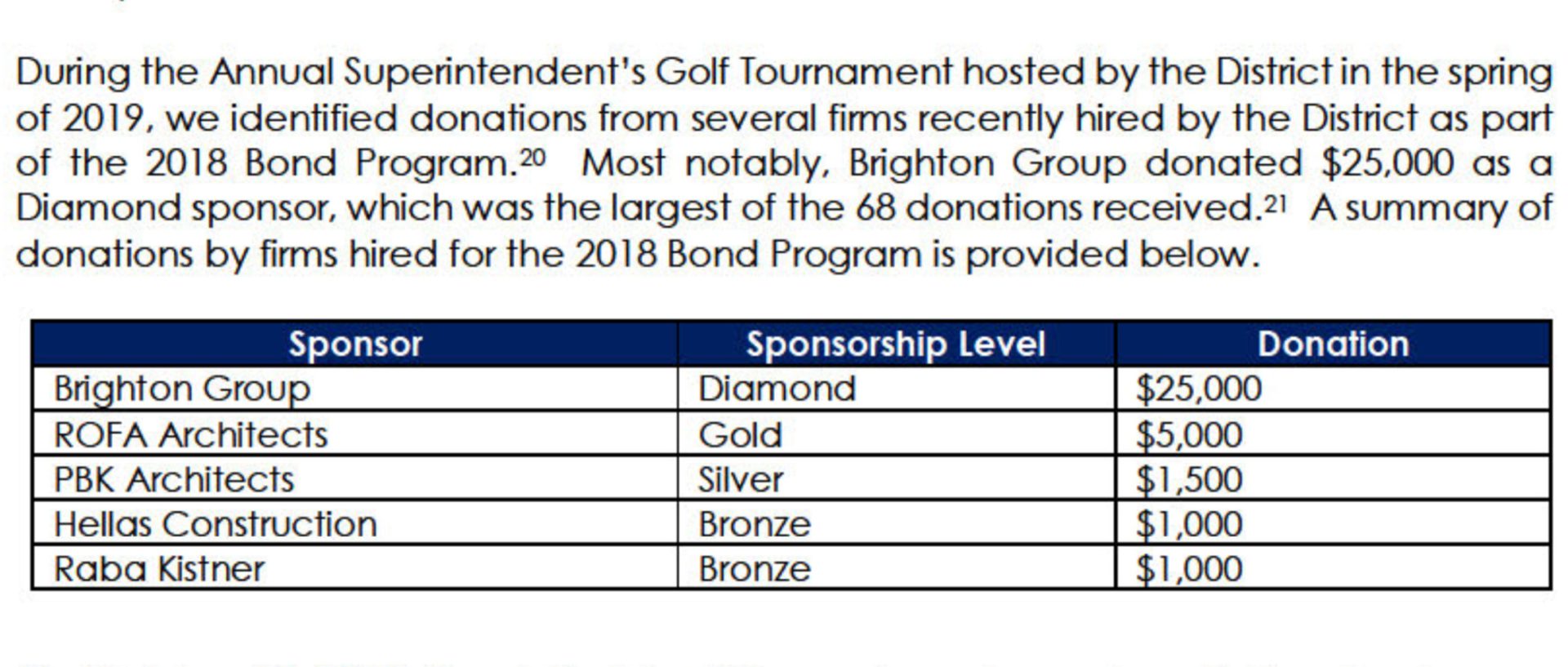

Auditors additionally noted that the Brighton Group was the biggest donor, contributing $25,000, to the district’s annual golf tournament in 2019.

“During the annual Superintendent’s Golf Tournament hosted by the district in the spring of 2019, we identified donations from several firms recently hired by the district as part of the 2018 bond program,” the report states. “Most notably, Brighton Group donated $25,000 as a diamond sponsor, which was the largest of the 68 donations received.”

In response, Palacios said his donation went to help fund scholarships for “disadvantaged children.”

“We have committed ourselves to be fabrics of the communities that we work in,” he said. “We donated checks which were written to SBCISD for the use of scholarships. That scholarship fund is managed by the district. We did all this with the heart to support community-based efforts in the San Benito area. There’s nothing wrong with offering contributions for scholarships for children.”

Palacios added he has also donated to the San Benito Rotary Club, the Callandret Black History Museum and the district’s convocation.

“It was done in great faith to help disadvantaged children or civic functions meant to provide positive impacts in the community,” he said.

CONSTRUCTION PROJECT’S COSTS

The audit included a review of the construction project aimed at building a performing arts theater, an aquatics center and an indoor practice field.

After the district gave the Brighton Group its contract in January 2021, the company completed work on the indoor practice field five months later, Palacios said.

Meanwhile, the project to build the performing arts theater and aquatics center, originally planned as running 18 to 24 months, was largely delayed as a result of the coronavirus pandemic’s disruption of the supply chain, he said, adding construction is expected to be completed next fall.

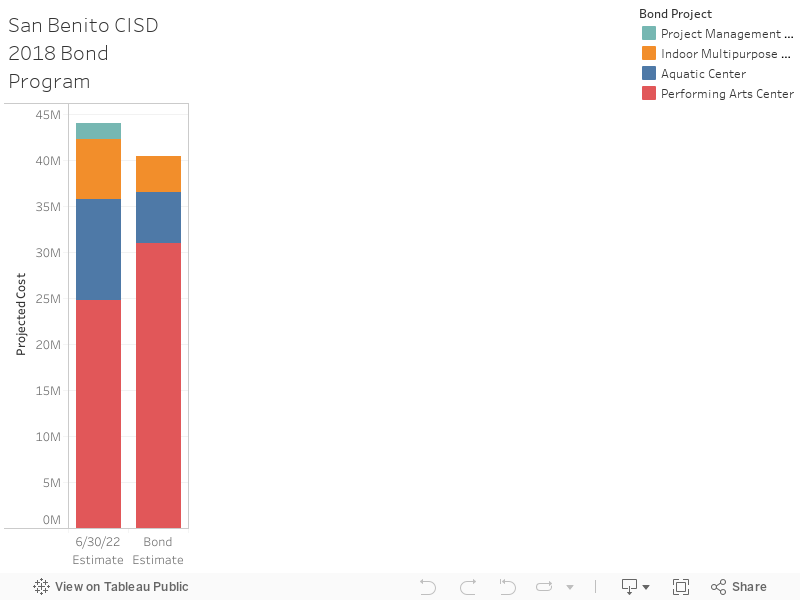

In their review, the auditor’s noted the project’s estimated cost increased from $40 million to $44 million.

“The cost estimates included in the bond proposition were based on estimated costs for similar facilities at other school districts in the area,” the report states. “The district did not hire outside consultants to assist in the preparation of the cost estimates during the pre-bond planning process. As a result, the cost estimates included in the $40 million bond proposition were rough estimates and did not account for site development costs, inflation or specific design plans that would be solicited by the district.”

In response, Palacios said the district chose not to hire consultants to save money in case voters rejected the bond proposal.

Later, he said, the school board requested a $1.8 million warm-up pool be included in the project to build an aquatics center.

“The board elected not to bring in a firm for pre-bond programming due to not being certain whether the bond would pass — they were being good stewards of their dollars,” Palacios said. “Other districts do that all the time. They don’t want to waste money if the bond doesn’t pass.”

Palacios said the coronavirus pandemic, which broke out a year later, disrupted the supply chain, driving up costs while limiting materials.

“None could ever have predicted COVID would ever come to light, that it would impact the construction activity as it did, which was materials escalation, depleted workforce and disruption of the supply chain,” he said.

PROJECT MANAGER’S SELECTION PROCESS

The audit also questioned the past school board’s selection process that led to its hiring of the Brighton Group.

“We observed a lack of transparency in the process that resulted in the board’s selection of the Brighton Group,” the report states.

The review found the board failed to evaluate qualifications, or “score,” four firms submitting proposals for the job, it states.

“We were unable to identify any documentation in support of the board’s evaluation” of proposals, the report states.

In response, Palacios said the board “ranked” the four firms, which included the Brighton Group, adding that neither school district policy nor the Texas Government Code require the board to “score” proposals.

“It does not specify that during the selection process they do anything more than evaluate the RFQ based on qualifications and experience,” Palacios said, referring to district policy. “In this case, the board did their due diligence in issuing an RFQ for this service. They did formal interviews with all firms in a public meeting with a full board and did site visits to projects of similar scope and they verified references. When they selected us, they took all that into consideration when they ranked us No. 1, so they did rank.”

“There was no violation of a government code, or their own policy or the RFQ process,” he added.

INSURANCE POLICY

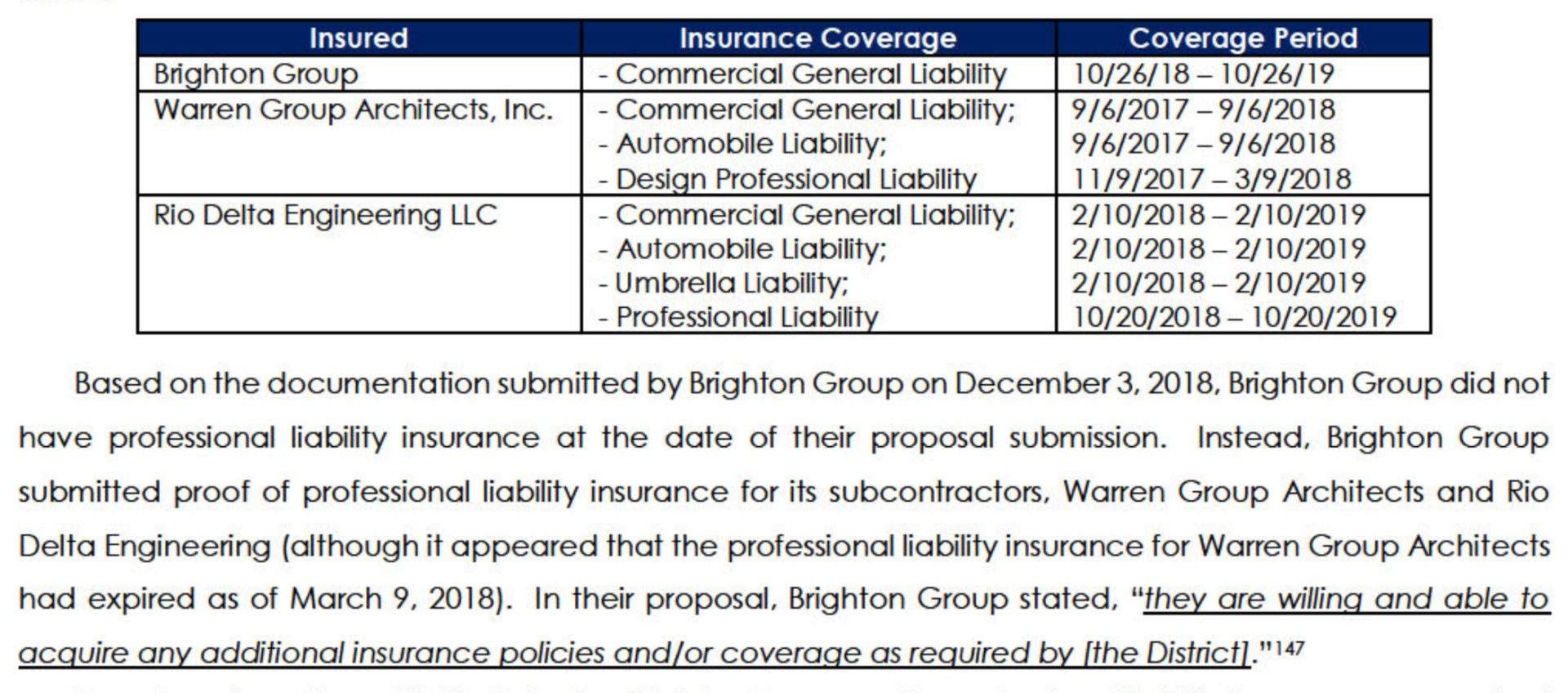

The audit also found the Brighton Group did not carry “appropriate” liability insurance required under Texas Government Code Section 2269.208, the report states.

“The district’s RFQ for project management services included a pre-requisite for the respondent to have appropriate liability insurance in accordance with Texas Government Code Section 2269.208. In their proposal submitted to the district on Dec. 3, 2018, Brighton Group did not provide documentation of professional liability policies required by the district. After the district’s selection of the Brighton Group on Dec. 18, 2018, Brighton Group obtained professional liability insurance coverage for the 2018 bond program effective Dec. 21, 2018.”

In response, Palacios said he followed “the traditional method” by obtaining the insurance after he was selected for the job on Dec. 21, 2018.

“The traditional method is you demonstrate the ability to have the required insurance, and that is specific to our RFQ, and once selected, a firm is required to issue a direct policy naming the entity (San Benito school district) as an additional insured and that all was done prior to any negotiations of a contract of Jan. 10, 2019,” he said.

Upon his firm’s selection for the job, he said, “he issued direct policy for professional liability with errors and omissions naming San Benito as the additional insured.”

Palacios added, “we always had professional liability insurance.”

ENGINEERING REGISTRATION

The auditors also noted the Brighton Group had not registered as a “professional engineering firm with the Texas Board of Professional Engineers and Land Surveyors until February 2019, which was after they entered into a contract with the district in January 2019.”

In response, Palacios said he responded to the district’s RFQ as a project management firm, not as an engineering service, adding his company included consulting engineers.

“Their RFQ was seeking qualifications for a project manager not engineering services,” Palacios said. “Our team had consulting engineers as well as architects that were not required in the RFQ.”

CONTRACT FEE

The audit noted the district paid the Brighton Group $1.25 million, an amount based on 4.5% of construction costs estimated at $3 million upon the contract’s inception.

“The contract outlined a payment schedule where Brighton Group was to receive $1.25 million, including $100,000 upon execution of the contract, followed by payments of $50,000 per month,” the report states. “As of December 2020, the Brighton Group had received $1.25 million in project management fees for the 2018 bond project based on the payment schedule outlined in the contract. However, the 2018 bond program is not scheduled for completion until August 2023 (at the earliest), which is 32 months after the last payment received by the Brighton Group.

“Based upon other reviews of other project management contracts at other school districts, fees are generally paid based on either project completion percentages each month, the completion of pre-determined milestones or based on hourly rates and time on the project. In our review, we did not identify any other project management contract where fees were paid in advance of services provided.”

In response, Palacios said his contracted fee was “not unusual.”

“They’re alluding the district pre-paid for services prior to the performance of services, which is completely incorrect,” he said. “The district developed our contract based on the program and the schedule. The scope of services in our contract clearly defines our levels of service from pre-design phase, design phase, construction document-phase and construction management phase.”

CMAR SELECTION PROCESS

The audit also raised questions surrounding the project’s Construction Manager at Risk services.

“The district procured Construction Manager at Risk (CMAR) services for the 2018 bond program through the issuance of an RFQ, prepared jointly by Brighton Group and the board’s attorney Tony Torres,” the report states. “Texas Government Code requires a two-step CMAR selection process if an entity elects to issue an RFQ instead of an RFP. It did not appear that the district completed the second step of the CMAR selection process as defined under the Texas Government Code.”

“The Texas Government Code requires the district to make public the ranking of submissions for CMAR services within seven days of a contract being awarded. We were unable to identify any documentation in support of the board’s evaluation process (e.g. rankings or score sheets), much less any documentation that was made public, which appears to be a violation of Texas Government Code. In October 2018, Hellas Construction contributed $1,000 to the special purpose acquisition company (SPAC) formed by members of the bond committee to raise funds to be used to promote the $40 million bond proposition. Hellas Construction was later selected as the CMAR for the construction of the indoor multi-purpose facility in May 2019.

In response, Palacios said state statute allows a one-step CMAR selection process.

“The statute says you can follow a one-step or a two-step,” he said. “The district went through the process of an RFQ. The district reviewed RFQs. They deliberated to do rankings in a public meeting. They started with negotiations of the contractor’s pre-construction services as well as the CMAR rate.”

At Hellas Construction’s Austin offices, Jeff Power, the company’s director of communications, declined comment, referring questions regarding the firm’s contribution to Sydney Stahlbaum, the company’s director of sales.

On Thursday, Stahlbaum was reviewing a message requesting comment.

PRICING REVIEW

The audit also found the district solicited five firms for an LED lighting project in which the Brighton Group reviewed pricing.

In June 2018, the district went out for bids, Palacios said.

Then in August 2018, the district reviewed the bids, he said.

After the district rescinded a contract with a company, it contracted with the Brighton Group to serve as project manager, requesting the firm “review and analyze the proposals submitted by E3 and Schneider Electric,” the report states.

“That was basically an analysis of the scope of work” regarding lighting fixtures, Palacios said. “The district has to do their due diligence. There were no new bids going out. Those bids had already been reviewed.”

SERVICES CONTRACT

The audit also included a review of the district’s 2018 $180,000 contract with the ABC Group, which produced a quarterly district newsletter suspended in October 2020 as a result of the coronavirus pandemic, the report states, adding the contract automatically extended for two years in 2021.

“We did not identify evidence of the board discussing the renewal,” the report states.

By the time the contract expires in April 2023, the district is expected to spend a total of $540,000 for public relations services from April 2018 to April 2023, it states.

MAINTENANCE AND OPERATIONS

The audit also included a review of a $2.1 million Parsons Commercial Roofing project “procured through a purchasing cooperative,” the report states.

In their review, the auditors found “it did not appear that other bids or quotes were obtained.”

Editor’s note: Board President Ramiro Moreno emailed a response to this story Sunday. Read it here.